CRM platform for increased sales in eCommerce, customer service, newsletters and chatbots

A multi-agent, all-in-one solution for businesses that sell products and services via WhatsApp, Facebook, Instagram, and websites on Shopify, WooCommerce, etc.

7 días gratis sin tarjeta de crédito ni compromisos

7 days free access, no credit cards or obligations

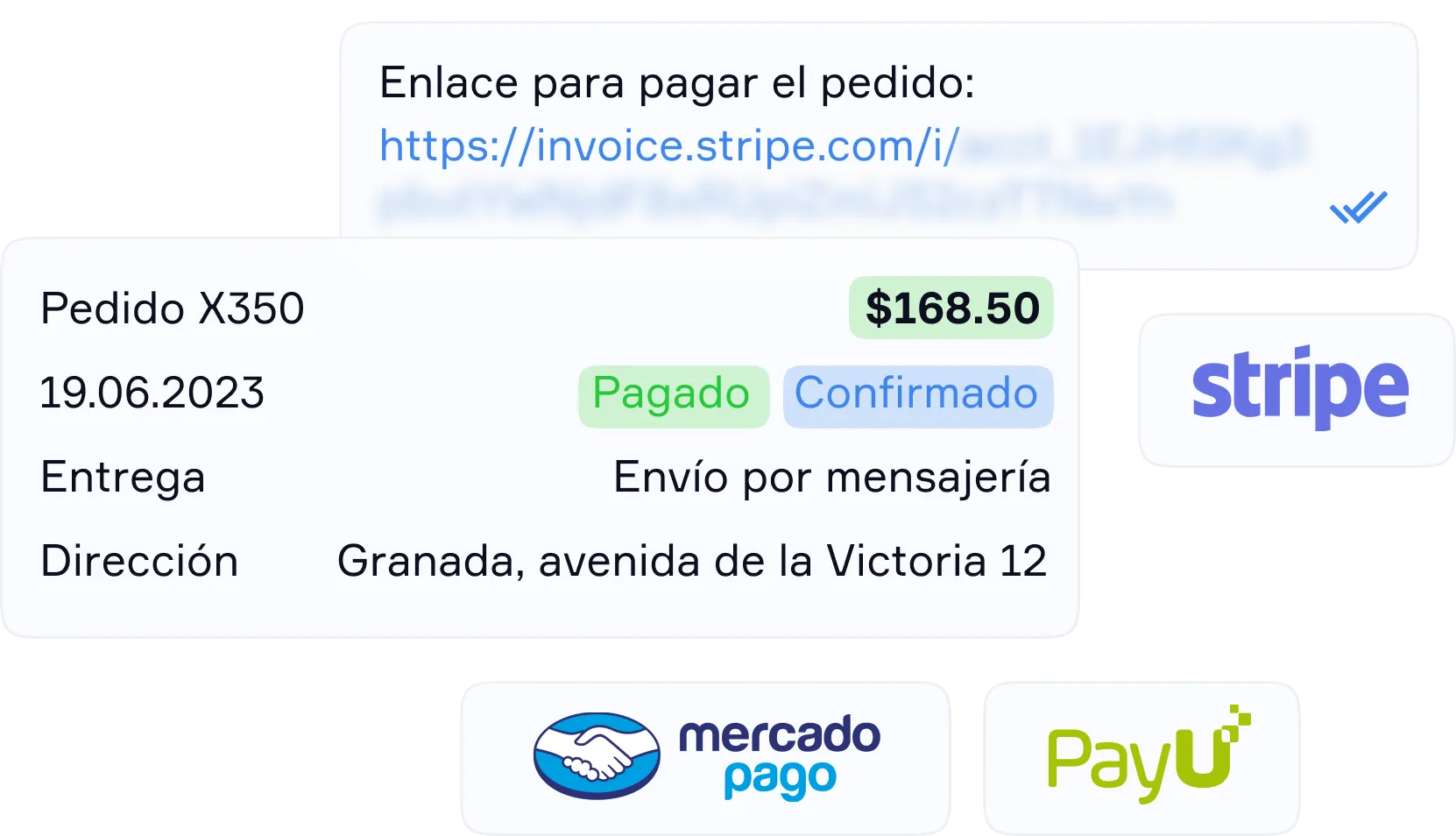

Create orders from the chat with your client

😱 Without leaving the conversation.

Simla.com allows you to give all your attention to the customer, reducing the need to use multiple systems.

Also, you'll be able to automatically save your potential customers to your database without any limitations, along with your conversation history. You can also distribute your orders and chats among your employees and monitor their real-time performance.

“Simla.com has helped us with our clients’ follow-up through effective information management. The ability to provide quick answers using fast 🚀 responses and to identify customers and their needs promptly has helped our clients place their trust 🤝 in us.”

Giovanni Mandracchia Corporate Financial Consultant

Boost your sales using promotional newsletters on WhatsApp Business

Harness the full potential of WhatsApp using Simla.com: Warm up your leads, reconnect with your clients, inform them about your sales, and more — without the risk of being blocked, thanks to an official API solution.

7 days free access, no credit cards or obligations

7 days free access, no credit cards or obligations

Simla.com costs less than losing a customer

Professional💥

3 users, one WhatsApp number, Facebook and Instagram, chatbots

+ Advanced analytics for chats and orders + WhatsApp newsletters and Email Marketing + CRM and sales funnel + Flexible segmentation of clients + ChatGPT to control your customer support + Ready-to-use modules to connect Shopify, PayPal, WooCommerce, etc.

.svg)

.svg)

Corporate Financial Consultant